Can You Buy a New Home Before Selling Your Current One?

The Louisville Homeowner's Guide to Bridge Loans, Equity Access, and Buy-Before-You-Sell Programs

Sometimes the right home appears before you're ready to sell the one you have.

Sometimes the call starts with excitement.

"We found the house."

Then comes the pause.

"But we haven't sold ours yet."

For many homeowners, this is the moment moving starts to feel impossible.

They finally find the right house. The neighborhood is right. The layout is right. The timing feels right.

But the equity they need for the next purchase is still locked inside their current home.

Suddenly the excitement of moving is replaced by a question:

Are we going to lose this house because we haven't sold ours yet?

This is one of the most common challenges homeowners face when trying to move from one home to another.

The good news is that selling first is not always the only option.

Depending on your finances, available equity, and lending qualifications, there may be several ways to purchase your next home before selling your current one.

Understanding those options can help you make decisions from a position of confidence rather than pressure.

If you're still trying to understand the overall process of selling and buying at the same time, start with our guide to moving without getting stuck between homes.

If you're still evaluating your overall moving strategy, start with our guide on How to Move Without Getting Stuck Between Homes.

Can You Buy a House Before Selling Yours?

Quick Answer

Yes.

Many homeowners purchase their next home before selling their current one.

The strategy typically involves one of four approaches:

• Qualifying for both homes simultaneously

• Using a bridge loan

• Accessing equity through a HELOC or home equity loan

• Using a specialized buy-before-you-sell program

The right solution depends on your financial situation, available equity, debt obligations, income, and lending qualifications.

The first step is understanding which options may be available before beginning the home search.

Why Homeowners Feel Stuck

The challenge is rarely a lack of equity.

The challenge is access.

Many Louisville homeowners have built significant equity over the past decade. In some cases, homeowners have hundreds of thousands of dollars available on paper.

The problem is that equity is not the same thing as cash.

Until the home is sold—or until financing is arranged against that equity—it can be difficult to use those funds toward another purchase.

This creates a frustrating situation.

A homeowner may have enough wealth to purchase the next home but not enough liquid funds to make it happen immediately.

That gap is where bridge financing and equity-access solutions enter the conversation.

What Most Homeowners Get Wrong About Buying Before Selling

Most homeowners assume there are only two choices:

• Sell first

• Stay where they are

In reality, the question is rarely whether a homeowner can move.

The question is whether they understand the financing tools available to support the move.

This is where many people unintentionally limit their options.

They spend months worrying about timing without first understanding what solutions may already be available.

The homeowners who experience the least stress are often not the ones with the most equity.

They are the ones who understand their choices before the perfect house appears.

A Common Louisville Scenario

Imagine a homeowner in Prospect who has lived in their home for more than a decade.

Their children are grown. They have built substantial equity. They have begun looking for a smaller home that better fits this next chapter of life.

Then they find it.

The problem is that their current home has not been listed yet.

They immediately assume they have two choices: rush to sell or let the opportunity go.

In reality, there may be other possibilities.

A conversation with a lender could reveal the ability to qualify for both homes, access equity through a HELOC, explore bridge financing, or investigate a buy-before-you-sell program.

The result is not necessarily purchasing before selling.

The result is understanding what is possible before making a decision.

That clarity often changes everything.

If you'd like to see additional examples of how Louisville homeowners navigate these decisions, read How Louisville Homeowners Successfully Sell and Buy at the Same Time.

Why This Matters More in Louisville's Competitive Neighborhoods

Buy-before-you-sell conversations become especially important when inventory is limited.

Homeowners targeting areas such as Prospect, Norton Commons, Anchorage, Lake Forest, Oldham County, and portions of Middletown often discover that suitable homes do not become available every day.

When opportunities are limited, flexibility can become valuable.

The ability to act when the right property appears may create options that would not otherwise exist.

This does not mean every homeowner should buy before selling.

It simply means understanding the available tools before timing becomes critical.

The Four Most Common Buy-Before-You-Sell Strategies

Most homeowners who purchase before selling use one of four approaches.

Each solves a different problem.

Each comes with different costs, risks, and advantages.

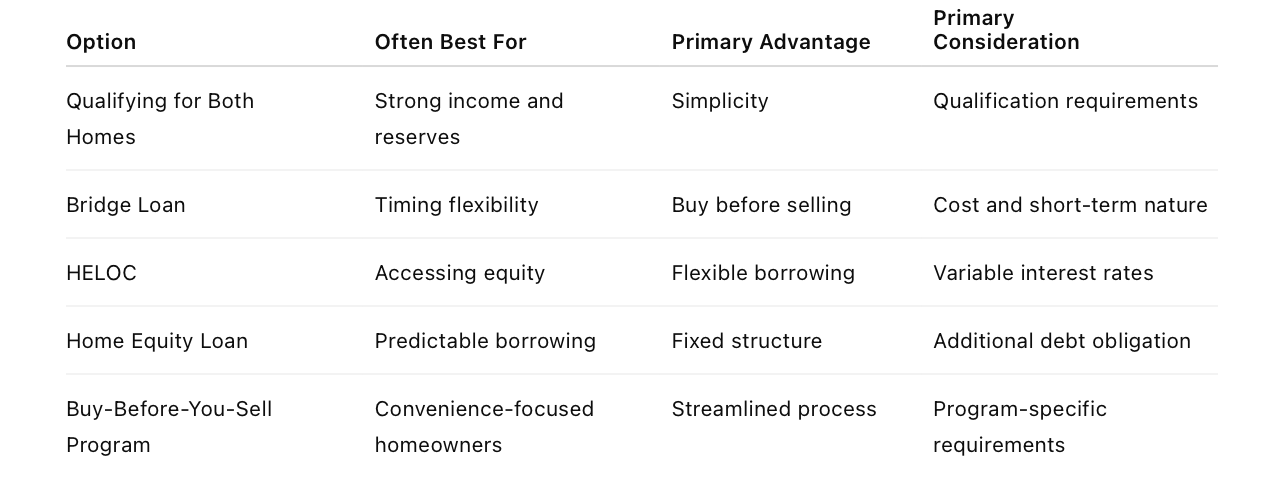

Option 1: Qualify for Both Homes

The simplest solution is often the least discussed.

Some homeowners can simply qualify for the new mortgage while still owning the current home.

This eliminates the need for bridge loans, special financing, or equity-access products.

Potential advantages include:

• Fewer moving parts

• Greater negotiating flexibility

• Ability to move before listing

• No pressure to sell immediately

Potential considerations include:

• Income requirements

• Debt-to-income ratios

• Reserve requirements

• Carrying two housing payments temporarily

This option generally works best for homeowners with strong income, manageable debt obligations, and sufficient reserves.

Option 2: Bridge Loans

Bridge loans are specifically designed to help homeowners purchase a new property before selling the current one.

As the name suggests, the financing creates a bridge between the purchase and the eventual sale.

Rather than waiting for the current home to close, homeowners may be able to use bridge financing to access funds needed for the next purchase.

Potential advantages include:

• Buying before selling

• Stronger purchase offers

• Reduced pressure during the transition

• More time to prepare the current home for market

Potential considerations include:

• Higher costs than traditional financing

• Additional qualification requirements

• Short-term repayment expectations

Bridge loans can be valuable tools when used appropriately, but they are not one-size-fits-all solutions.

They are often most effective when paired with a thoughtful timeline strategy for coordinating both transactions.

Option 3: Home Equity Lines of Credit (HELOCs)

A HELOC allows homeowners to borrow against available equity through a revolving line of credit.

Unlike a lump-sum loan, funds can often be accessed as needed during the approved draw period.

Potential advantages include:

• Flexible access to equity

• Interest paid only on amounts used

• Potential down payment source

• May remain available after the move

Potential considerations include:

• Qualification requirements

• Variable interest rates

• Additional monthly obligations

Many homeowners explore HELOCs before listing because approval can become more complicated once the property is actively being marketed for sale.

Option 4: Home Equity Loans

A home equity loan provides a lump sum secured by available equity.

Unlike a HELOC, the amount is received upfront and repaid according to the loan terms.

Some homeowners prefer the predictability of a fixed payment structure.

Others prefer the flexibility of a line of credit.

The right choice depends on how the funds will be used and the homeowner's broader financial goals.

What Is a Bridge Loan?

A bridge loan is a short-term financing product designed to provide temporary access to funds while a homeowner transitions between properties.

The loan is typically repaid when the current home sells.

Think of it as temporary access to equity that has not yet been converted into cash through a sale.

For some homeowners, a bridge loan creates flexibility.

For others, alternative solutions may be more practical.

The best approach depends on the overall financial picture.

What Are Buy-Before-You-Sell Programs?

In recent years, several lenders have introduced specialized programs designed specifically for homeowners caught between transactions.

These programs vary significantly by lender.

Depending on the provider, they may offer:

• Temporary financing

• Equity advances

• Cash-offer programs

• Delayed sale options

• Bridge-style lending structures

The goal is generally the same:

Allow homeowners to secure the next home before finalizing the sale of the current one.

Availability, costs, requirements, and risks vary widely, which is why lender-specific conversations are essential.

Comparing Buy-Before-You-Sell Options

Which Option Fits Your Situation?

If your priority is simplicity, qualifying for both homes may be worth exploring.

If your priority is accessing equity, a HELOC or home equity loan may deserve consideration.

If your priority is securing a specific property before it disappears from the market, bridge financing may provide additional flexibility.

If your priority is convenience and reducing logistical complexity, a buy-before-you-sell program may be attractive.

The best solution depends less on the product itself and more on the problem you are trying to solve.

Can You Access All of Your Equity?

Not necessarily.

Many homeowners assume they can automatically borrow against all available equity.

In reality, lenders typically evaluate:

• Current mortgage balance

• Estimated home value

• Debt-to-income ratio

• Income and employment

• Credit profile

• Available cash reserves

The amount that can be accessed varies significantly from one homeowner to another.

This is why early planning matters.

The goal is understanding your options before you need them.

How This Fits Into Your Overall Moving Plan

Financing is only one piece of the puzzle.

The bigger challenge is coordinating the entire transition.

Understanding bridge loans, HELOCs, home equity loans, and buy-before-you-sell programs becomes far more valuable when paired with a thoughtful strategy for timing the sale and purchase.

Likewise, seeing how other Louisville homeowners have successfully navigated these decisions can provide perspective and confidence.

The goal is not simply finding financing.

The goal is creating a move that feels manageable.

Financing is only one piece of the puzzle. Coordinating timelines, possession dates, and closing schedules is equally important when selling one home and buying another.

Frequently Asked Questions

Can I buy a house before selling my current house?

Yes. Depending on your finances, you may qualify for both homes simultaneously, use a bridge loan, access home equity, or use a specialized buy-before-you-sell program.

How much equity do I need to buy another home?

There is no universal amount. Available equity, lender requirements, debt obligations, and income all influence what options may be available.

What is a bridge loan?

A bridge loan is short-term financing designed to help homeowners purchase a new home before their current home sells.

Is a HELOC better than a bridge loan?

Neither is inherently better. They solve different problems and work best in different situations.

Can I use home equity as a down payment?

In some cases, yes. A lender can help determine what options may be available based on your situation.

Should I buy before selling?

It depends on your finances, risk tolerance, available inventory, and overall moving goals.

Thinking About Moving But Unsure Where to Start?

Most homeowners do not need financing advice first.

They need clarity first.

Understanding your home's value, available equity, likely sale timeline, and potential financing options creates a much stronger foundation for decision-making.

A planning conversation before you begin house hunting can often reveal opportunities you did not realize existed.

The earlier you understand your options, the more flexibility you typically have when the right home appears.

Final Thoughts

Many homeowners assume they cannot move until their current home sells.

That is sometimes true.

But often, there are more options available than they realize.

Bridge loans, HELOCs, home equity loans, and buy-before-you-sell programs all exist because homeowners face this challenge every day.

The goal is not finding the perfect financing product.

The goal is creating enough flexibility that you can make a good housing decision without feeling trapped by timing.

Because moving should be driven by your goals.

Not by fear.