How Louisville Homeowners Successfully Sell and Buy at the Same Time

See how Louisville homeowners navigate real-world moving challenges using coordinated closings, rent-back agreements, financing strategies, and flexible timelines to move with confidence.

Real-Life Moving Scenarios, Timing Strategies, and What These Transitions Actually Look Like

The best moves are rarely perfect. They are simply planned well enough to move forward with confidence.

Most homeowners want to know if it is possible.

Can you really sell one home and buy another without everything falling apart?

Can the closings line up?

Can you avoid moving twice?

Can you make a strong offer before your current home is fully behind you?

The answer is yes.

It can happen.

But it does not happen because everyone gets lucky.

It happens because the move is planned as one connected transition instead of two separate transactions.

I understand how important these decisions can feel because I have had to navigate similar moving logistics in my own life. As a parent of four young children, I know firsthand that a move affects far more than a house. It affects routines, schedules, work, school, childcare, and the people depending on you.

That is one reason I believe so strongly in planning.

The goal is not perfect timing.

The goal is creating enough clarity that your next step feels manageable.

Sometimes closings line up beautifully, even back to back. Sometimes the better solution is a rent-back agreement, bridge financing, a flexible closing date, or a short-term backup plan.

The important thing to understand is this:

There is not one right way to sell and buy at the same time.

There is only the right strategy for the homeowner, the property, the financing, the market, and the timing.

The examples below are based on common situations Louisville homeowners face. They are not intended to identify specific clients. They are meant to show what this process can look like when the pieces are handled thoughtfully.

Can You Sell and Buy a Home at the Same Time in Louisville?

Quick Answer

Yes.

Many Louisville homeowners sell their current home and buy their next home during the same overall transition.

Some homeowners close both transactions on the same day. Others close a few days apart, negotiate post-closing possession, use a rent-back agreement, or buy first with financing support.

The right structure depends on your equity, financing, risk tolerance, target neighborhood, and how much flexibility exists on both sides of the move.

The goal is not always perfect timing.

The goal is a plan that protects your next step.

If you're looking for a complete overview of the process, start with our guide on moving without getting stuck between homes.

What Successful Sell-and-Buy Transitions Have in Common

The smoothest moves usually begin before a sign ever goes in the yard.

That may sound simple, but it is often the difference between a stressful move and a manageable one.

Successful homeowners usually understand their likely equity position, have spoken with a lender early, know where they want to move, and have talked through what happens if timing does not unfold perfectly.

They do not assume the sale and purchase will magically align.

They prepare for several possible outcomes.

That preparation creates confidence long before the first showing or offer.

What Most Homeowners Get Wrong About Coordinated Closings

Many homeowners assume the ideal outcome is closing on the sale and purchase at the exact same time.

Sometimes that is possible.

I have seen closings line up back to back, with one sale funding the next purchase in a way that feels almost seamless.

But that is not always possible.

And it is not always the only successful outcome.

A successful move may involve closing on the sale first and remaining in the home briefly through a negotiated possession agreement. It may involve buying first and selling shortly afterward. It may involve adjusting closing dates to create breathing room for everyone involved.

The mistake is believing there is only one version of success.

There are often several

Understanding how timelines, possession dates, and closing schedules work together can often make these decisions much easier.

The Move Everyone Hopes For

Most homeowners imagine the same outcome.

The proceeds from one home fund the purchase of the next.

The sale closes.

The purchase closes.

The move happens.

Life moves forward.

And sometimes that is exactly what happens.

A homeowner prepares their current property carefully, identifies the next home early, and works through inspections, financing, and contract deadlines with a clear plan. The timing aligns. The sale funds the purchase. The transition feels remarkably smooth.

From the outside, it can look effortless.

It rarely is.

What appears seamless is usually the result of weeks of planning, communication, lender coordination, title work, inspections, and contingency preparation happening behind the scenes.

When back-to-back closings work, they are often the result of preparation rather than luck.

When Selling First Felt Safer

Another common situation involves a homeowner who feels confident selling but uncertain about what comes next.

Maybe inventory is limited.

Maybe the next move is highly specific.

Maybe they need proceeds from the sale but do not want to rush into the wrong purchase.

In these situations, selling first often creates financial clarity.

The challenge is creating enough time to find the next home without feeling pressured.

Sometimes a negotiated possession period or rent-back agreement becomes the bridge between those two goals.

Instead of moving out immediately after closing, the seller remains in the home for an agreed period while completing the next step.

When structured correctly, this approach can provide valuable breathing room and reduce the pressure that often leads to rushed decisions.

When the Perfect House Appeared Too Soon

Sometimes the next home shows up before the current home is sold.

This is often where anxiety spikes.

The homeowner knows the house is right.

The location works.

The layout works.

The timing suddenly feels urgent.

The challenge is that the current home has not yet sold.

This is where preparation matters most.

Some homeowners can qualify while still owning their current home. Others may explore bridge loans, home equity solutions, or buy-before-you-sell programs.

The specific solution matters less than the lesson.

The best time to understand your options is before the perfect house appears.

Once emotions are high and deadlines are short, decision-making becomes much harder.

Homeowners in this situation often explore bridge loans, HELOCs, home equity loans, and buy-before-you-sell programs before deciding on their next step.

When Flexibility Became the Better Plan

Not every successful move is perfectly synchronized.

Sometimes the best strategy is not precision.

Sometimes the best strategy is flexibility.

A few extra days between closings may make the transition smoother. A possession agreement may create breathing room. Temporary housing, while not always ideal, may protect a homeowner from rushing into a purchase that is not quite right.

This is particularly true when the next home search is highly specific.

A homeowner searching for a patio home, acreage, a first-floor primary suite, a particular school district, or a specific Louisville neighborhood may benefit more from flexibility than from forcing a rigid timeline.

The goal is not perfection.

The goal is protecting the decision.

The Pattern Beneath Every Successful Move

Although the details change, the pattern rarely does.

The homeowners who move most successfully are not necessarily the wealthiest.

They are not always the luckiest.

They are rarely the ones with perfect market conditions.

They are usually the ones who begin planning before pressure arrives.

They understand their equity.

They understand their financing.

They understand the realities of the neighborhoods where they hope to buy.

Most importantly, they understand that a successful move is not created by perfect timing.

It is created by having options when timing changes.

Why Local Market Conditions Matter

A coordinated move in Louisville is not only about your home.

It is also about the home you hope to buy next.

A homeowner selling in a neighborhood with strong demand may be able to negotiate more favorable timing than someone selling in a slower segment of the market.

A buyer searching in areas such as Prospect, Anchorage, Norton Commons, Lake Forest, Middletown, or Oldham County may face limited inventory depending on price point and property type.

That changes the strategy.

If your current home is likely to sell quickly but your next home may take time to find, the plan needs to account for that.

If the next home is available but your current home is not yet ready, the plan needs to account for that too.

The strongest strategy is never based on one side of the move.

It is based on both.

The Four Things That Shape Every Moving Strategy

Before deciding whether to sell first, buy first, or coordinate both transactions, homeowners usually need clarity in four areas.

Money.

Timing.

Inventory.

Flexibility.

Do you need proceeds from your current home to purchase the next one?

Can you qualify before selling?

How difficult will the next home be to find?

How much flexibility exists if timelines shift unexpectedly?

Most moving decisions eventually come back to those four things.

Once those questions are answered, the path forward often becomes much clearer.

How to Avoid Moving Twice

Quick Answer

The best way to avoid moving twice is to plan the sale and purchase together before listing or making an offer.

Common strategies include coordinated closing dates, rent-back agreements, post-closing possession, flexible contract timelines, bridge financing, and buy-before-you-sell programs.

Not every strategy works for every homeowner.

The right option depends on financing, equity, market conditions, and the willingness of all parties to negotiate timing.

What Can Go Wrong If There Is No Plan?

Without a plan, homeowners often find themselves making decisions under pressure.

They may accept an offer without thinking through possession.

They may list before understanding financing options.

They may find the right home but not know whether they can act.

They may assume temporary housing is the only solution.

They may attempt to align two closings without accounting for delays.

None of these situations means the move cannot work.

But they can make the process feel far more stressful than it needs to be.

Planning does not eliminate every challenge.

It simply creates more options when challenges appear.

Frequently Asked Questions

Can you close on selling and buying a house on the same day?

Yes. Same-day or back-to-back closings are possible, but they require careful coordination between all parties involved.

What happens if my sale closing is delayed?

A delay can affect the purchase closing, moving schedule, or possession timeline. This is why contingency planning is important.

Can I stay in my house after selling it?

Sometimes. A rent-back or post-closing possession agreement may allow a seller to remain in the home for a limited period after closing.

Is it better to sell first or buy first?

It depends on your finances, equity, target market, and risk tolerance. There is no universal answer.

How do I avoid temporary housing?

Common strategies include coordinated closings, rent-back agreements, flexible possession terms, bridge financing, or buying before selling.

Can a Realtor help coordinate both closings?

Yes. An experienced agent can help structure timelines, communicate with lenders and title companies, negotiate possession terms, and keep both transactions moving together.

Thinking About Selling and Buying at the Same Time?

If you are considering a move, the first conversation should not only be about what your home is worth.

It should also be about where you are going next.

A thoughtful planning conversation can help clarify your equity, timing, financing options, target neighborhoods, and backup plans before pressure enters the picture.

Every move is different.

But the homeowners who feel most confident are usually the ones who understand their options before they need them.

That clarity can make all the difference.

Final Thoughts

Coordinating a sale and purchase is possible.

I have seen closings line up beautifully, even back to back.

I have also seen situations where the better solution was a rent-back agreement, a flexible closing date, or a different timing strategy altogether.

The point is not to force every move into the same shape.

The point is to create a plan that fits the real life around it.

Because a successful move is not always the one that looks perfect on paper.

It is the one that gets you from where you are to where you are going with as much clarity, care, and steadiness as possible.

How to Coordinate Selling and Buying a Home at the Same Time

Learn how Louisville homeowners coordinate selling one home while buying another. Discover timeline strategies, closing date planning, rent-back agreements, and practical ways to reduce stress and avoid a double move.

The Louisville Homeowner's Guide to Timelines, Closing Dates, and Avoiding a Double Move

The smoothest moves usually begin with a plan long before closing day arrives.

Most homeowners think the biggest challenge is finding the next house.

It usually isn't.

The biggest challenge is timing.

The right home appears.

Your current home receives an offer.

Inspections are scheduled.

Lenders begin working.

Moving companies need dates.

Suddenly, what seemed like one decision becomes dozens.

Will your home sell before the next one is ready?

What happens if both closings don't line up?

Should you close on the purchase first?

Should you close on the sale first?

Will you need temporary housing?

Will you have to move twice?

These are the questions that create stress.

Not because something is wrong.

Because moving involves multiple events that rarely happen on the exact same timeline.

The good news is that homeowners successfully coordinate these transitions every day.

The key is understanding how the process works before the deadlines arrive.

If you're still deciding whether to sell first, buy first, or coordinate both transactions, start with our guide on How to Move Without Getting Stuck Between Homes.

How Do You Sell and Buy a Home at the Same Time Without Moving Twice?

Quick Answer

Most successful transitions involve three things:

• Planning before listing

• Building flexibility into contracts

• Creating backup plans before they are needed

The homeowners who experience the least stress are rarely the ones whose transactions unfold perfectly.

They are the ones who prepare for multiple outcomes.

Whether your goal is buying before selling, selling before buying, or coordinating both closings, the most important step is creating a realistic timeline before major decisions are made.

The Three Questions That Determine Your Timeline

Before deciding when to buy or sell, most homeowners need answers to three questions.

Do I need proceeds from my current home to purchase the next one?

How quickly are homes selling in the area where I want to buy?

How flexible am I if timelines do not align perfectly?

Those three answers often determine everything that follows.

A homeowner who can qualify before selling may have far more flexibility than someone who needs proceeds from their current home. Likewise, someone searching in a neighborhood with limited inventory may face a different challenge than someone moving into an area with more available options.

Most timeline decisions become much clearer once these questions are answered.

Why Timing Creates More Stress Than Selling

Most homeowners spend significant time thinking about pricing, repairs, staging, and negotiations.

Few spend enough time thinking about logistics.

Yet logistics are often what create the greatest anxiety.

The concern usually sounds something like this:

"What if my house sells too fast?"

Or:

"What if I find the perfect house too soon?"

Or:

"What if everything happens at the same time?"

These concerns are understandable.

When people think about moving, they often imagine a straight line.

In reality, most moves involve multiple overlapping timelines. Preparing a home for sale, searching for the next property, inspections, financing, appraisals, packing, utility transfers, and closing coordination are all moving simultaneously.

The goal is not making every timeline identical.

The goal is creating enough flexibility that they can work together.

What Most Homeowners Get Wrong About Timing

Many homeowners believe success means making the sale and purchase close on the exact same day.

While that can happen, it is rarely the true goal.

The goal is reducing stress.

Sometimes that means a same-day closing.

Sometimes it means a rent-back agreement.

Sometimes it means a few extra days between transactions.

Sometimes it means temporary housing.

The homeowners who struggle most are often pursuing perfection.

The homeowners who move most confidently are usually pursuing flexibility.

That distinction changes everything.

What Causes Most Moving Timelines to Change?

Most delays are not caused by major problems.

They are caused by ordinary events that occur in real estate transactions every day.

An inspection uncovers an issue that requires additional discussion. An appraiser needs more time. A lender requests documentation. Title work reveals a question that needs clarification. A contractor's schedule shifts. A moving company is booked further out than expected.

These situations are common.

Understanding that reality helps homeowners prepare realistically rather than assuming every delay signals a failing transaction.

In many cases, a timeline adjustment is simply part of the normal process.

A Common Louisville Scenario

The stress did not begin when the family listed their Middletown home.

It began when they found the next one.

The neighborhood felt right. The house felt right. The timing suddenly felt urgent.

At first, their focus was entirely on securing the property.

Then the questions started.

What if their current home sold immediately?

What if inspections created delays?

What if the seller requested a longer closing?

What if they needed possession before their sale closed?

The challenge was not finding the home.

The challenge was understanding the timeline.

What ultimately helped was not finding a perfect solution.

It was creating several workable ones.

That experience is common across Louisville.

A homeowner moving from Lake Forest into a patio home faces a different challenge than a buyer searching for limited inventory in Prospect, Anchorage, Norton Commons, Middletown, or Oldham County.

The strongest timeline plans account for both sides of the move.

Understanding your current home's likely marketability is important.

Understanding the realities of your target market is equally important.

This is one example of a challenge Louisville homeowners face. Other successful transitions often follow different paths depending on timing, financing, and inventory.

The Three Most Common Timing Strategies

Most homeowners follow one of three paths.

Each can work.

Each has trade-offs.

Sell First, Then Buy

Selling first creates the greatest financial certainty.

You know your proceeds. You understand your available equity. You know exactly what budget you can comfortably use for the next purchase.

The trade-off is timing.

If the right home has not appeared yet, temporary housing or additional flexibility may be necessary.

For homeowners who value certainty above convenience, this approach often makes the most sense.

Buy First, Then Sell

Buying first allows homeowners to secure the next property before letting go of the current one.

This can reduce pressure during the home search and may create a smoother overall transition.

The challenge is financing.

Some homeowners qualify carrying both properties. Others explore bridge loans, HELOCs, home equity loans, or buy-before-you-sell programs.

The right solution depends on the homeowner's finances, available equity, and overall goals.

Many homeowners pursuing this strategy explore bridge loans, HELOCs, home equity loans, or buy-before-you-sell programs before making a move.

Coordinate Both Transactions

This is the approach many homeowners hope to achieve.

The goal is aligning the sale and purchase closely enough to create a seamless transition.

When successful, this can minimize disruption and reduce the likelihood of moving twice.

It typically requires more coordination, but it can also create one of the smoothest overall experiences.

The Planning Timeline Most Homeowners Should Follow

One of the easiest ways to reduce stress is starting earlier than you think necessary.

Approximately three to four months before moving, homeowners should begin evaluating their home's value, understanding their equity position, discussing financing if necessary, and identifying both preferred neighborhoods and realistic backup options.

Roughly two to three months before moving, attention shifts toward preparation. This is often when repairs, decluttering, staging discussions, and contractor work begin taking shape.

As the move approaches, timelines begin to overlap. Listing preparation, active home searching, financing updates, and vendor coordination often happen simultaneously.

Once contracts are involved, communication becomes the priority. Inspections, appraisals, financing milestones, utility transfers, and moving logistics all begin working together.

The homeowners who remain calm during this phase are usually the ones who planned before reaching it.

Stress-Test Your Plan Before You List

One of the most valuable exercises homeowners can complete is testing their plan before it is needed.

What if your home sells during the first weekend?

What if it takes sixty days to find the next property?

What if your preferred neighborhood has no available inventory?

What if inspections create delays?

What if closing dates do not align?

What if temporary housing becomes necessary?

If you have answers before these situations occur, you are already ahead of most homeowners.

The goal is not predicting the future.

The goal is reducing the number of surprises that can create stress later.

Tools That Help Avoid a Double Move

Many homeowners fear moving twice more than almost any other part of the process.

Fortunately, several tools may help reduce that risk.

A rent-back agreement may allow a seller to remain in the home after closing, creating additional time to secure the next property.

Flexible closing dates can sometimes create breathing room between transactions.

Some homeowners use bridge financing or equity-access solutions to purchase before selling.

Others discover that short-term housing, while not ideal, provides more flexibility and less pressure than forcing two transactions to align perfectly.

The best solution depends on the circumstances.

The common thread is flexibility.

Which Timing Strategy Fits Your Situation?

If your primary concern is financial certainty, selling first may deserve consideration.

If your primary concern is securing a specific property, buying first may create flexibility.

If your primary concern is avoiding multiple moves, coordinated closings and possession planning may be worth exploring.

The best timing strategy is not necessarily the most efficient one.

It is the one that creates the most manageable transition for your situation.

The Homeowner's Timeline Checklist

Before listing, understand your likely proceeds, financing options, preferred neighborhoods, and acceptable backup plans.

Before accepting an offer, think through possession needs, replacement housing options, and how much flexibility exists if timelines shift unexpectedly.

Once under contract, communication becomes the priority. Inspections, financing, moving schedules, utility transfers, and closing coordination all begin working together.

The homeowners who experience the least stress are usually the ones who make decisions early rather than waiting until deadlines force them to.

How This Fits Into Your Overall Moving Plan

Timing is only one piece of a successful transition.

Understanding financing options may expand flexibility.

Understanding how other Louisville homeowners have navigated these same challenges often provides perspective and confidence.

Most importantly, understanding the entire sell-and-buy process creates clarity.

The goal is not controlling every variable.

The goal is preparing for the variables you cannot control.

Frequently Asked Questions

How do I avoid moving twice?

Many homeowners use rent-back agreements, coordinated closings, flexible possession periods, or buy-before-you-sell strategies to reduce the likelihood of moving twice.

Should I buy first or sell first?

It depends on your finances, risk tolerance, available inventory, and overall goals.

What happens if my home sells before I find another one?

Potential solutions may include rent-back agreements, temporary housing, delayed closings, or alternative financing options.

How far apart should closing dates be?

There is no universal answer. The ideal timing depends on your goals, financing, and flexibility needs.

What is a rent-back agreement?

A rent-back agreement allows a seller to remain in the property for a period after closing.

How early should I start planning?

Most homeowners benefit from beginning the planning process at least sixty to one hundred twenty days before they hope to move.

Thinking About Moving?

Most homeowners do not need a perfect timeline.

They need a realistic one.

Understanding your home's likely marketability, your financing options, your target neighborhoods, and your flexibility points can dramatically reduce stress later.

The best time to create a moving plan is before you need one.

Because options are usually greatest before deadlines appear.

Final Thoughts

Most homeowners believe successful moves happen because everything unfolds perfectly.

More often, they happen because homeowners prepare thoughtfully before the pressure arrives.

Closing dates shift.

Inspections uncover surprises.

Inventory changes.

Lenders request additional documentation.

That is normal.

The goal is not creating a timeline that never changes.

The goal is creating enough flexibility that a change in timing does not change the decision.

Because moving should feel intentional.

Not rushed.

Can You Buy a New Home Before Selling Your Current One?

Found the right house before selling your current one? Learn how Louisville homeowners use bridge loans, HELOCs, home equity loans, and buy-before-you-sell programs to create more flexibility when moving.

The Louisville Homeowner's Guide to Bridge Loans, Equity Access, and Buy-Before-You-Sell Programs

Sometimes the right home appears before you're ready to sell the one you have.

Sometimes the call starts with excitement.

"We found the house."

Then comes the pause.

"But we haven't sold ours yet."

For many homeowners, this is the moment moving starts to feel impossible.

They finally find the right house. The neighborhood is right. The layout is right. The timing feels right.

But the equity they need for the next purchase is still locked inside their current home.

Suddenly the excitement of moving is replaced by a question:

Are we going to lose this house because we haven't sold ours yet?

This is one of the most common challenges homeowners face when trying to move from one home to another.

The good news is that selling first is not always the only option.

Depending on your finances, available equity, and lending qualifications, there may be several ways to purchase your next home before selling your current one.

Understanding those options can help you make decisions from a position of confidence rather than pressure.

If you're still trying to understand the overall process of selling and buying at the same time, start with our guide to moving without getting stuck between homes.

If you're still evaluating your overall moving strategy, start with our guide on How to Move Without Getting Stuck Between Homes.

Can You Buy a House Before Selling Yours?

Quick Answer

Yes.

Many homeowners purchase their next home before selling their current one.

The strategy typically involves one of four approaches:

• Qualifying for both homes simultaneously

• Using a bridge loan

• Accessing equity through a HELOC or home equity loan

• Using a specialized buy-before-you-sell program

The right solution depends on your financial situation, available equity, debt obligations, income, and lending qualifications.

The first step is understanding which options may be available before beginning the home search.

Why Homeowners Feel Stuck

The challenge is rarely a lack of equity.

The challenge is access.

Many Louisville homeowners have built significant equity over the past decade. In some cases, homeowners have hundreds of thousands of dollars available on paper.

The problem is that equity is not the same thing as cash.

Until the home is sold—or until financing is arranged against that equity—it can be difficult to use those funds toward another purchase.

This creates a frustrating situation.

A homeowner may have enough wealth to purchase the next home but not enough liquid funds to make it happen immediately.

That gap is where bridge financing and equity-access solutions enter the conversation.

What Most Homeowners Get Wrong About Buying Before Selling

Most homeowners assume there are only two choices:

• Sell first

• Stay where they are

In reality, the question is rarely whether a homeowner can move.

The question is whether they understand the financing tools available to support the move.

This is where many people unintentionally limit their options.

They spend months worrying about timing without first understanding what solutions may already be available.

The homeowners who experience the least stress are often not the ones with the most equity.

They are the ones who understand their choices before the perfect house appears.

A Common Louisville Scenario

Imagine a homeowner in Prospect who has lived in their home for more than a decade.

Their children are grown. They have built substantial equity. They have begun looking for a smaller home that better fits this next chapter of life.

Then they find it.

The problem is that their current home has not been listed yet.

They immediately assume they have two choices: rush to sell or let the opportunity go.

In reality, there may be other possibilities.

A conversation with a lender could reveal the ability to qualify for both homes, access equity through a HELOC, explore bridge financing, or investigate a buy-before-you-sell program.

The result is not necessarily purchasing before selling.

The result is understanding what is possible before making a decision.

That clarity often changes everything.

If you'd like to see additional examples of how Louisville homeowners navigate these decisions, read How Louisville Homeowners Successfully Sell and Buy at the Same Time.

Why This Matters More in Louisville's Competitive Neighborhoods

Buy-before-you-sell conversations become especially important when inventory is limited.

Homeowners targeting areas such as Prospect, Norton Commons, Anchorage, Lake Forest, Oldham County, and portions of Middletown often discover that suitable homes do not become available every day.

When opportunities are limited, flexibility can become valuable.

The ability to act when the right property appears may create options that would not otherwise exist.

This does not mean every homeowner should buy before selling.

It simply means understanding the available tools before timing becomes critical.

The Four Most Common Buy-Before-You-Sell Strategies

Most homeowners who purchase before selling use one of four approaches.

Each solves a different problem.

Each comes with different costs, risks, and advantages.

Option 1: Qualify for Both Homes

The simplest solution is often the least discussed.

Some homeowners can simply qualify for the new mortgage while still owning the current home.

This eliminates the need for bridge loans, special financing, or equity-access products.

Potential advantages include:

• Fewer moving parts

• Greater negotiating flexibility

• Ability to move before listing

• No pressure to sell immediately

Potential considerations include:

• Income requirements

• Debt-to-income ratios

• Reserve requirements

• Carrying two housing payments temporarily

This option generally works best for homeowners with strong income, manageable debt obligations, and sufficient reserves.

Option 2: Bridge Loans

Bridge loans are specifically designed to help homeowners purchase a new property before selling the current one.

As the name suggests, the financing creates a bridge between the purchase and the eventual sale.

Rather than waiting for the current home to close, homeowners may be able to use bridge financing to access funds needed for the next purchase.

Potential advantages include:

• Buying before selling

• Stronger purchase offers

• Reduced pressure during the transition

• More time to prepare the current home for market

Potential considerations include:

• Higher costs than traditional financing

• Additional qualification requirements

• Short-term repayment expectations

Bridge loans can be valuable tools when used appropriately, but they are not one-size-fits-all solutions.

They are often most effective when paired with a thoughtful timeline strategy for coordinating both transactions.

Option 3: Home Equity Lines of Credit (HELOCs)

A HELOC allows homeowners to borrow against available equity through a revolving line of credit.

Unlike a lump-sum loan, funds can often be accessed as needed during the approved draw period.

Potential advantages include:

• Flexible access to equity

• Interest paid only on amounts used

• Potential down payment source

• May remain available after the move

Potential considerations include:

• Qualification requirements

• Variable interest rates

• Additional monthly obligations

Many homeowners explore HELOCs before listing because approval can become more complicated once the property is actively being marketed for sale.

Option 4: Home Equity Loans

A home equity loan provides a lump sum secured by available equity.

Unlike a HELOC, the amount is received upfront and repaid according to the loan terms.

Some homeowners prefer the predictability of a fixed payment structure.

Others prefer the flexibility of a line of credit.

The right choice depends on how the funds will be used and the homeowner's broader financial goals.

What Is a Bridge Loan?

A bridge loan is a short-term financing product designed to provide temporary access to funds while a homeowner transitions between properties.

The loan is typically repaid when the current home sells.

Think of it as temporary access to equity that has not yet been converted into cash through a sale.

For some homeowners, a bridge loan creates flexibility.

For others, alternative solutions may be more practical.

The best approach depends on the overall financial picture.

What Are Buy-Before-You-Sell Programs?

In recent years, several lenders have introduced specialized programs designed specifically for homeowners caught between transactions.

These programs vary significantly by lender.

Depending on the provider, they may offer:

• Temporary financing

• Equity advances

• Cash-offer programs

• Delayed sale options

• Bridge-style lending structures

The goal is generally the same:

Allow homeowners to secure the next home before finalizing the sale of the current one.

Availability, costs, requirements, and risks vary widely, which is why lender-specific conversations are essential.

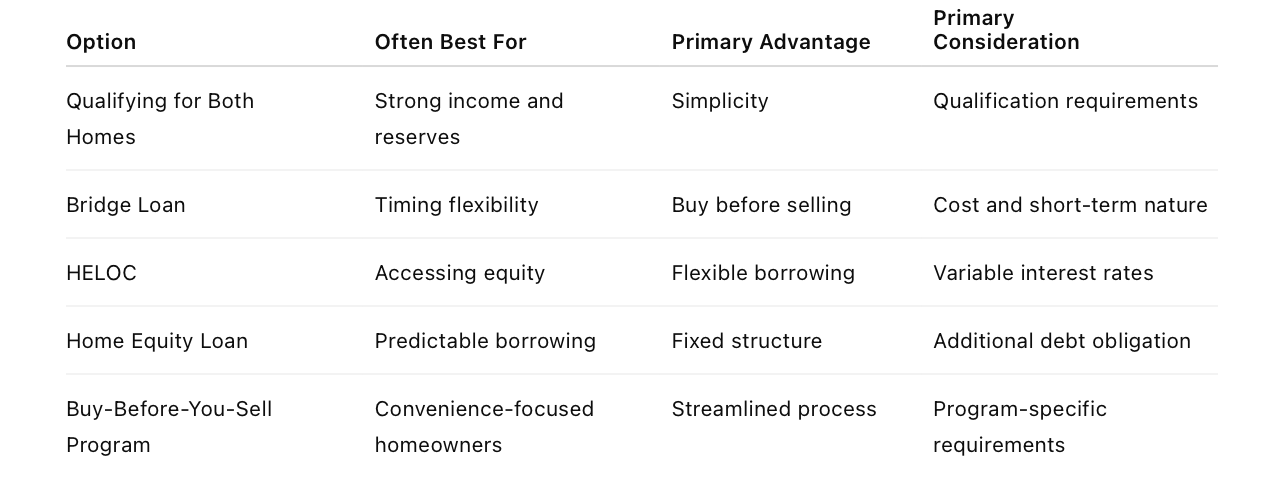

Comparing Buy-Before-You-Sell Options

Which Option Fits Your Situation?

If your priority is simplicity, qualifying for both homes may be worth exploring.

If your priority is accessing equity, a HELOC or home equity loan may deserve consideration.

If your priority is securing a specific property before it disappears from the market, bridge financing may provide additional flexibility.

If your priority is convenience and reducing logistical complexity, a buy-before-you-sell program may be attractive.

The best solution depends less on the product itself and more on the problem you are trying to solve.

Can You Access All of Your Equity?

Not necessarily.

Many homeowners assume they can automatically borrow against all available equity.

In reality, lenders typically evaluate:

• Current mortgage balance

• Estimated home value

• Debt-to-income ratio

• Income and employment

• Credit profile

• Available cash reserves

The amount that can be accessed varies significantly from one homeowner to another.

This is why early planning matters.

The goal is understanding your options before you need them.

How This Fits Into Your Overall Moving Plan

Financing is only one piece of the puzzle.

The bigger challenge is coordinating the entire transition.

Understanding bridge loans, HELOCs, home equity loans, and buy-before-you-sell programs becomes far more valuable when paired with a thoughtful strategy for timing the sale and purchase.

Likewise, seeing how other Louisville homeowners have successfully navigated these decisions can provide perspective and confidence.

The goal is not simply finding financing.

The goal is creating a move that feels manageable.

Financing is only one piece of the puzzle. Coordinating timelines, possession dates, and closing schedules is equally important when selling one home and buying another.

Frequently Asked Questions

Can I buy a house before selling my current house?

Yes. Depending on your finances, you may qualify for both homes simultaneously, use a bridge loan, access home equity, or use a specialized buy-before-you-sell program.

How much equity do I need to buy another home?

There is no universal amount. Available equity, lender requirements, debt obligations, and income all influence what options may be available.

What is a bridge loan?

A bridge loan is short-term financing designed to help homeowners purchase a new home before their current home sells.

Is a HELOC better than a bridge loan?

Neither is inherently better. They solve different problems and work best in different situations.

Can I use home equity as a down payment?

In some cases, yes. A lender can help determine what options may be available based on your situation.

Should I buy before selling?

It depends on your finances, risk tolerance, available inventory, and overall moving goals.

Thinking About Moving But Unsure Where to Start?

Most homeowners do not need financing advice first.

They need clarity first.

Understanding your home's value, available equity, likely sale timeline, and potential financing options creates a much stronger foundation for decision-making.

A planning conversation before you begin house hunting can often reveal opportunities you did not realize existed.

The earlier you understand your options, the more flexibility you typically have when the right home appears.

Final Thoughts

Many homeowners assume they cannot move until their current home sells.

That is sometimes true.

But often, there are more options available than they realize.

Bridge loans, HELOCs, home equity loans, and buy-before-you-sell programs all exist because homeowners face this challenge every day.

The goal is not finding the perfect financing product.

The goal is creating enough flexibility that you can make a good housing decision without feeling trapped by timing.

Because moving should be driven by your goals.

Not by fear.

How to Move Without Getting Stuck Between Homes

Thinking about selling your current home while buying another? Learn the three most common ways Louisville homeowners make a move, plus strategies for timing, equity, contingencies, rent-back agreements, and avoiding the stress of getting stuck between homes.

The Louisville Homeowner's Guide to Selling and Buying at the Same Time

Most successful moves begin with a plan long before the first sign goes in the yard.

Most homeowners who contact me about moving have already made the decision emotionally.

They simply have not figured out the logistics yet.

The house may no longer fit their lifestyle. The maintenance may feel heavier than it once did. A growing family may need more space, while an empty nester may be caring for rooms that rarely get used. Sometimes the home still works perfectly well, but life has changed around it.

The challenge is rarely deciding whether a move makes sense.

The challenge is figuring out how to move from one home to another without creating unnecessary stress along the way.

What happens if your home sells before you find another one? What if you find the right home before yours sells? Can you use your equity to buy before selling? Will you have to move twice?

These questions cause many homeowners to delay decisions they may otherwise be ready to make.

The good news is that homeowners successfully navigate this transition every day. The key is understanding your options before making the first move.

Can You Sell and Buy a Home at the Same Time?

Quick Answer

Yes.

Most Louisville homeowners who move are selling one home while purchasing another. Depending on their finances and timeline, the transition may involve coordinated closing dates, sale contingencies, rent-back agreements, bridge financing, or other equity-access strategies.

The key is creating a plan before your current home goes on the market.

How Do You Sell and Buy a Home at the Same Time?

Most Louisville homeowners accomplish this in one of three ways:

• Sell first, then buy

• Buy first, then sell

• Coordinate both transactions through timing strategies such as contingencies, rent-back agreements, or bridge financing

The right approach depends on your available equity, financing options, timeline, and the availability of homes in your target area.

While every situation is different, homeowners who plan the transition before listing their home typically have more flexibility and experience less stress throughout the process.

What This Looks Like in Louisville Right Now

One reason homeowners feel stuck is that today's market does not fit neatly into old assumptions.

Many Louisville homeowners have built significant equity over the last several years. At the same time, inventory remains limited in many popular neighborhoods and price ranges.

As a result, selling may not be the difficult part.

Finding the right next home may be.

A homeowner moving from a larger home in Lake Forest into a patio home faces a different challenge than a growing family trying to move into Middletown, Prospect, Oldham County, Norton Commons, or another highly sought-after area.

In many of these areas, homeowners can sell successfully and still struggle to find the right replacement property simply because available inventory remains limited.

The strongest plans are built around the realities of your specific move, not broad headlines about the market.

Understanding both sides of the transition—your current home's likely sale and your next home's availability—is often where clarity begins.

What If You Have a Low Mortgage Rate?

Quick Answer

A low mortgage rate should be part of the decision.

It should not become the entire decision.

Many homeowners who purchased or refinanced several years ago have mortgage rates that would be difficult to replace today. That reality deserves consideration.

At the same time, a home is more than a financing tool.

It is supposed to support the life being lived inside it.

If your current home still fits your needs, staying may be the right choice.

If your home no longer fits your lifestyle, family needs, maintenance preferences, or long-term goals, then the conversation becomes larger than an interest rate.

The homeowners who gain the most clarity often stop asking, "Can I get this rate again?" and start asking, "What am I gaining by staying, and what am I giving up?"

That is usually where the real answer begins.

The Decision Is Usually Easier Than the Process

Most homeowners know whether they want to move long before they know how they want to move.

The decision often becomes clear through everyday life. A home feels too large, too small, too far away, too much work, or simply out of sync with the season of life someone is in.

What creates hesitation is rarely the decision itself.

It is the process.

Once homeowners understand the available paths forward, many discover the move is more manageable than they originally imagined.

Good planning does not eliminate every surprise.

It simply replaces uncertainty with options.

What Most Homeowners Get Wrong About Moving

Many homeowners believe the biggest challenge is selling their current home.

In reality, the bigger challenge is often creating a realistic plan for the next one.

The homeowners who experience the least stress typically spend more time planning the transition than preparing the property for sale.

They understand where their equity stands, how financing may work, what neighborhoods they want to target, and what backup plans exist if timing does not unfold exactly as expected.

The goal is not creating a perfect plan.

The goal is creating enough clarity that decisions become easier when opportunities arise.

The Three Ways Most Homeowners Make a Move

Most homeowners who sell and buy at the same time follow one of three broad paths. Each can work. Each has trade-offs. The best choice depends on your finances, timeline, and priorities.

Sell First, Then Buy

Selling first creates the greatest financial certainty.

You know how much equity you have available, what your proceeds will likely look like, and what budget you can comfortably use for the next purchase.

The trade-off is timing.

If your home sells before you find another one, you may need temporary housing, storage, or additional flexibility.

For homeowners who value financial clarity above all else, this approach often makes the most sense.

Buy First, Then Sell

Buying first allows you to secure the next home before letting go of the current one.

This approach can reduce the pressure of finding a replacement property quickly, especially if your housing needs are very specific.

The challenge is financing.

Depending on your situation, you may need bridge financing, access to home equity, or the ability to qualify while still owning your current home.

For homeowners considering this path, it helps to understand the various buy-before-you-sell programs, bridge financing options, and equity-access strategies that may be available.

For homeowners with strong equity positions and stable finances, this can be an effective option.

Coordinate Both Transactions

This is the approach many homeowners hope to achieve.

The goal is to align the sale and purchase so you can move once, minimize disruption, and create a smoother transition.

This often involves coordinating closing dates, negotiating possession timelines, or using tools such as rent-back agreements.

It typically requires more planning, but it can create the least stressful overall experience.

Thoughtful planning around timelines, possession dates, and contingency periods can often eliminate the need for temporary housing or a double move.

If your biggest concern is timing rather than financing, you may also find our guide on coordinating closing dates and avoiding a double move helpful.

What Happens If My Home Sells Before I Find Another One?

This is one of the most common concerns homeowners have.

The good news is that several options may exist.

Depending on your situation, you may be able to negotiate a longer closing period, use a rent-back agreement, arrange temporary housing, or delay listing until your purchase strategy becomes clearer.

The important thing is discussing these possibilities before they happen.

A strong plan does not assume everything will line up perfectly.

It prepares for multiple outcomes.

What Happens If I Find the Right Home Before Mine Sells?

The opposite concern can feel just as stressful.

Sometimes the right home appears before the current home has sold. When that happens, preparation becomes valuable.

Possible solutions may include a sale contingency, bridge financing, home equity access, a longer closing timeline, or qualifying to purchase before selling.

The right solution depends on your finances, the competitiveness of the home you want to buy, and the likely marketability of your current home.

Planning ahead creates more options than reacting under pressure.

What Is a Sale Contingency?

A sale contingency allows a buyer to purchase a home only if their current home sells successfully.

In practical terms, it provides financial protection.

Rather than being obligated to purchase a new home regardless of what happens with the old one, the contingency creates a safeguard.

The trade-off is that some sellers may prefer offers without contingencies.

Whether a sale contingency makes sense depends on the market, the property, and the strength of the overall offer.

Sale contingencies are often discussed alongside rent-back agreements, but they solve very different problems. A sale contingency helps address a financing concern, while a rent-back agreement helps address a timing concern.

Like many real estate tools, a sale contingency is neither good nor bad. It simply serves a specific purpose.

What Is a Rent-Back Agreement?

A rent-back agreement allows a seller to remain in the home for a period after closing.

If a sale contingency helps solve a financial challenge, a rent-back agreement helps solve a timing challenge.

For homeowners trying to avoid moving twice, this can be one of the most useful tools available.

A properly structured rent-back can provide additional time to purchase the next home, coordinate movers, finish packing, or avoid temporary housing altogether.

The details matter, which is why these agreements should be carefully documented and negotiated.

Can You Use Your Equity Before Selling?

Many homeowners have substantial equity but cannot easily access it until their home sells.

Depending on your financial situation, there may be several options worth discussing with a lender.

One common misconception is that all available equity can automatically be used toward the next purchase. In reality, lenders evaluate factors such as loan-to-value ratios, credit profile, income, existing obligations, and the amount of equity available.

The amount a homeowner can access varies significantly from one situation to another.

This is why conversations with both a lender and real estate professional are often helpful before making decisions about timing.

For homeowners exploring bridge loans, HELOCs, home equity loans, or buy-before-you-sell programs, our guide to buying a new home before selling your current one explores these options in greater detail.

Bridge Loans

Bridge loans provide short-term financing designed to help homeowners purchase a new property before the current home sells.

Home Equity Line of Credit (HELOC)

A HELOC may allow access to available equity before the home is sold, creating additional flexibility during the transition.

Home Equity Loan

A home equity loan provides a lump sum secured by the equity in the home.

Buy-Before-You-Sell Programs

Some lenders offer specialized programs designed to help homeowners purchase before selling.

Every option carries different requirements, costs, and risks. A lender can help determine which solutions may be appropriate for your situation.

The First Conversation to Have Before You List

Most homeowners assume the first step is preparing the house.

Often, it is not.

The first step is understanding the move.

Before listing, it helps to answer several important questions:

• Do I need the proceeds from my current home to purchase the next one?

• Can I qualify before selling?

• How flexible am I on timing?

• What type of home am I hoping to buy?

• What would I do if my home sold in the first week?

• What would I do if it took longer than expected to find the next home?

You do not need perfect answers.

You simply need enough clarity to understand your available options.

That conversation alone often removes much of the uncertainty that causes homeowners to feel stuck.

A Common Louisville Scenario

Imagine a homeowner in Lake Forest who purchased their home when their children were in elementary school.

Twelve years later, one child is in college and another is preparing to leave home. Entire rooms sit unused. The yard requires more maintenance than they enjoy. Travel has become a bigger priority than square footage.

The challenge is not selling the home.

The challenge is deciding how to move into something smaller without creating unnecessary disruption.

Before listing, they review their home's value, estimate their available equity, speak with a lender, and identify the type of home they hope to buy next. They discuss timing, contingency options, and backup plans before the first showing ever takes place.

The result is not a perfect transaction.

It is a predictable one.

And predictable usually feels far better than stressful.

You can also see how these strategies play out in real-world situations in How Louisville Homeowners Successfully Sell and Buy at the Same Time.

Frequently Asked Questions

How do I sell and buy a home at the same time?

By treating both transactions as one coordinated transition and creating a plan before listing or making an offer.

Should I sell before buying?

It depends on whether financial certainty or timing flexibility matters most in your situation.

Can I buy before mine sells?

Possibly. Some homeowners can qualify before selling, while others may need bridge financing or access to home equity.

What is a sale contingency?

A contract provision that makes a purchase dependent on the successful sale of the buyer's current home.

What is a rent-back agreement?

An agreement that allows a seller to remain in the home for a period after closing.

How early should I start planning?

Most homeowners benefit from beginning the planning process 60 to 120 days before they hope to move.

Thinking About Making a Move?

If you're considering selling one home while buying another, the first step is understanding your options before you list.

A planning conversation can help clarify:

• Your available equity

• Potential financing options

• Timing strategies

• Backup plans if the market changes

• What your current home is likely to sell for

• What opportunities may exist in your target area

Every move is different, but the goal is the same: creating a path forward that fits your life, finances, and timeline.

Final Thoughts

Many homeowners believe the hardest part of moving is selling their home.

More often, the hardest part is understanding how all the pieces fit together.

The good news is that you do not have to solve every piece at once.

You simply need a plan.

The homeowners who move with the most confidence are rarely the ones who perfectly time the market. They are the ones who understand their options before making decisions.

If you are considering a move, start there.

Not with packing.

Not with a sign in the yard.

Start with a clearer understanding of your path forward.

The goal is not finding the perfect strategy.

It is finding the strategy that helps you move forward with confidence.

Because your move deserves care, not chaos.